Cross-company director performance evaluation: a thought experiment

Investors might have an appetite to hold directors accountable, not just on a single board but across all their board roles, according to data from a recent Glass Lewis survey. Although the survey doesn’t focus specifically on North American investors—most relevant for the US market —it indicates that 79% of global investors and 36% of North American respondents (investor + non-investor) would consider penalizing directors for poor performance across multiple boards. Wow!

Surprisingly, a “cross-company director performance score” hasn't emerged yet, but it seems inevitable. The real question is: would cross-company director performance evaluations fundamentally change Board culture and decision-making? And is that good or bad?

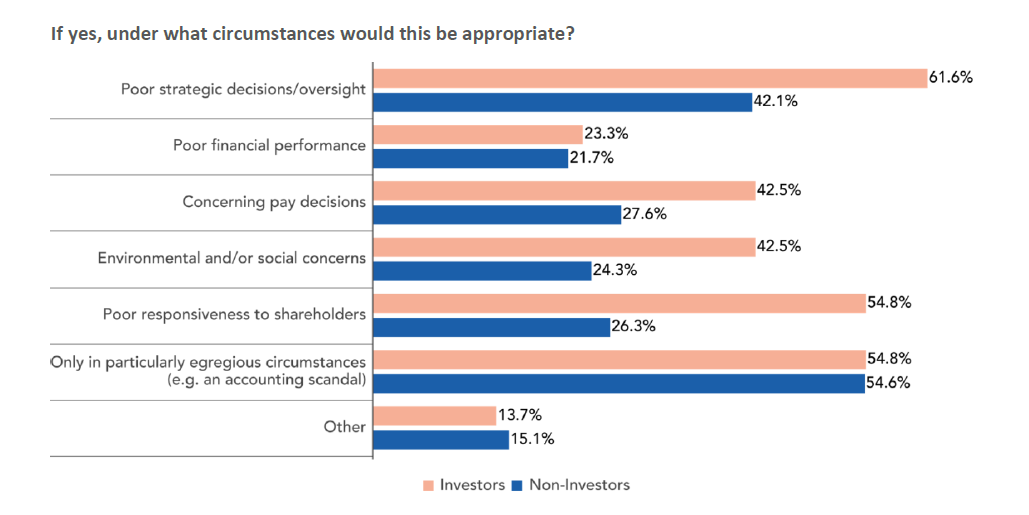

A screenshot that expands on the Glass Lewis results further below:

If investors were to track directors across all their board assignments and evaluate their performance, vote outcomes, and governance practices at those companies, it could help them establish person-by-person governance profiles and determine who is good at the job. A cross-company view is rarely used in the director election process, but it could be a better way to build boards.

The good and the bad of “cross-company director performance evaluations”

The approach would turbo-charge the role of reputation in the boardroom. Reputation is a mighty force on boards already. Directors are often motivated by prestige, influence, and network value, not solely compensation. Being associated with a poorly managed or governed company can be embarrassing and an undercurrent that influences the board's decision-making for better or worse. Harnessing the power of reputation through a system that highlights alignment—or lack thereof—with investor governance preferences across Boards could rapidly influence governance norms.

That said, it would be naive to pretend investor governance preferences are universally applicable in every situation. Directors want to be perceived as effective stewards of shareholder capital. Still, their job is to make wise choices amidst tension between competing priorities, which sometimes means bucking the governance norms and doing what’s right for the company and shareholders. The risk of a cross-company performance evaluation is that it could make it harder for directors to focus on substance over reputation.

Nowhere is that tension on display more than in the Say on Pay world. Pay issues arise most frequently during moments of crisis: poor performance, retention concerns, and investor frustrations. Price declines trip proxy advisor wires while causing retention and motivation challenges for an executive team at the same time. Investor preferences don’t always make space for what the Company needs during times of crisis. Wise stewardship sometimes means going headfirst into a Say on Pay issue because it’s the right thing for the company. A recent example from my clients:

A poor-performing company with a one-year PSU metric knew it would receive poor Say on Pay results (poor performance + a one-year metric that doesn’t conform to proxy advisor preferences). The Company could have garnered shareholder support by moving to a multi-year measure. Its executive team was in turmoil following two key exits. The Board chose to stay the course with its pay design and provided one executive with a special grant, knowing they would experience Say on Pay failure because the retention and motivation issues were too dire to risk. It was the right choice to stabilize the team.

Say on Pay votes are non-binding, but repeated failures can jeopardize director positions and demand resource-intensive remediation involving shareholder outreach and compensation redesigns. Directors try to avoid failures, except when prioritizing company needs over investor preferences becomes essential. Directors that have failed Say on Pay have some reputational hit, but it’s modest. Because there is pretty widespread acceptance that the norms around executive pay don’t always create smart business outcomes, there’s a pretty high level of tolerance around Say on Pay issues before it starts to impact someone’s reputation more broadly.

A major challenge with 'cross-company director performance scores' is the lack of nuance. Any crude evaluation wouldn’t be able to differentiate between misaligned investor preferences and deliberate, strategic governance choices. Overemphasis on governance reputation risks stifling directors' ability to take calculated risks or exercise sound judgment. So the debate here becomes: Is harnessing reputation as a tool for corporate governance a good or bad thing? Do we want faster, more responsive, responsible governance, or is the risk of perverse incentives where directors prioritize reputation management over substance too large?

So, where do I stand on this thought experiment?

In my opinion, it’s not that deep. If investors can accurately identify which directors excel in the job and which don’t, that's a positive development. However, investors should be cautious not to amplify the existing flaws in compensation and governance frameworks. Take Say on Pay, for instance. It's fraught with issues and doesn’t always capture the complexities of board decisions. I would love it if the investor and proxy advisor preferences around Say on Pay were more universally logical, but they aren’t, and labeling someone a “bad” director based solely on a Say on Pay failure is reductive. But if someone was involved in genuinely bad governance practices, why not let that be a stain? Cross-company director performance scores should emphasize genuine performance and be discerning in which framework to consider.