Pay for Last Year’s Performance

The long-standing and awkward timing tension at the center of proxy advisor pay versus performance reviews

Proxy advisors face a complicated task, and I don’t blame them for using the frameworks they do. Given the sheer volume of companies and the nuances involved in executive compensation, it makes sense that proxy advisors lean on standardized approaches like their quantitative pay for performance assessments. But anyone who works in corporate governance, executive pay, or sits on a compensation committee knows that the proxy advisor frameworks are not a silver bullet. This post focuses on one of the most basic challenges in proxy advisor evaluations: timing.

The core pay-for-performance framework that proxy advisors rely on is awkward because there is a delay between when Boards (j) make decisions and (ii) disclose those decisions. It’s not dramatic - the corporate governance world has lived with the disconnect for 15 years since the start of Say on Pay - but it is enough to confuse decision-making and push boards towards relying more on art than science when establishing executive pay. I think it is worth asking: Is there a better way?

The Timing Problem Explained

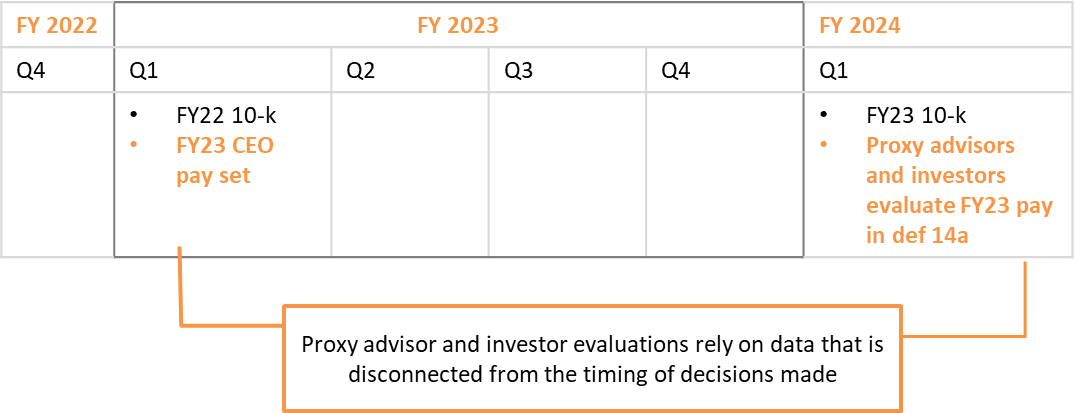

Simply put, companies disclose CEO compensation one full year after the Board decides what to pay the CEO. That delay means proxy advisors evaluate pay outcomes against performance results that don’t reflect the context in which those decisions were made. Instead, they evaluate performance that occurred after the fact—a full year after the fact. The table below outlines the typical CEO pay decision-making timeline.

When Say on Pay was first introduced, some speculated that companies might shift the timing of their pay decisions to December rather than January or February (for a 12/31 company). The idea was that decisions made in December would better align with the financial results they were associated with. But that shift never happened. Boards decide on CEO pay in January/February because they need the year-end results to inform the decision. The only exception to this practice is in the financial services industry (the industry uses a “total rewards” model that leans more heavily on bonuses). Still, for all other industries, there is a mismatch between the decisions the boards make and the time frame proxy advisors use to evaluate those decisions. Investors and Boards just live with it.

The timing disconnect is challenging for Boards striving to achieve a genuine connection between pay and performance. When performance outcomes for a year are known, it’s been nearly ten months since the pay decisions were made.

Illustrative Example of the Dilemma:

- A company experienced mixed performance in FY20, so the Board decided to hold the CEO pay flat the next year aka a decision made in FY21 Q1

- Performance improved considerably that year (FY21), and the peer market data shifted dramatically. The Board wanted to make a bigger increase to CEO pay for FY22 Q1, to reflect that FY21 performance

- That FY22 Q1 increase wouldn’t hit the proxy tables until the next year in Q1 FY23 Q1, but the Board did not know how performance would land for the full FY22 year, which would also be reported in Q1 FY23

- Meanwhile, FY21 CEO pay, which was set following the FY20 performance year, would show up in the proxy statement side by side with the stronger FY21 result; take a look:

- The Board faced a decision of whether to (a) make a quick adjustment to CEO pay in FY21 before the year closed, so the increase “hit the tables” in FY22 Q1 and aligned with performance to limit the risk of a mismatch the following year, or (b) live with the uncertainty of not knowing how the numbers will look the next year.

The fact that this is a familiar and very common dilemma boards face each year is troubling. They grapple with prioritizing genuine pay-for-performance alignment or focusing on managing how it will be perceived. Unfortunately, those two things are often at odds with one another. Many boards are left throwing up their hands, thinking, "I hope we got it right" The timing disconnect disempowers boards, undermines the goals of pay-for-performance, and diminishes the influence of proxy advisors. Instead of engaging thoughtfully with ISS and Glass Lewis’ evaluations, boards often tweak their practices just enough to avoid scrutiny rather than fully embracing the principles. If I were an investor, I’d want proxy advisors to assess how thoughtful and responsive a board’s decision-making process was, not whether the disclosures lined up perfectly.

Recent Developments in Proxy Advisor Policies

To be clear, I don’t fault the proxy advisors - they need consistent and repeatable frameworks. However, their frameworks can sometimes lead to unintended consequences, complicating things for boards genuinely committed to a performance-driven philosophy. There also is space for them to continue to evolve and refine their perspective because they are ultimately guided by their investors’ perspectives, which seems to be at the beginning of their own evolutions.

Both ISS and Glass Lewis recently released their updates for the 2025 proxy season, hinting at potential future shifts. Glass Lewis, for example, signaled an increased focus on evaluating actual payout decisions, not just program structures. ISS hasn’t substantially changed its policies but left the door open for further exploration in 2026. Both firms seem to be inching toward a more nuanced and practical approach to pay-for-performance evaluations.

A Modest Proposal for Better Pay Evaluations

What if proxy advisors shifted their focus? Two potential paths:

- Companies could do a better job describing the context that led to their decisions (i.e., performance from the prior year), and proxy advisors could take that into consideration in their evaluations. Companies don’t currently take this point head-on in their public filings, and they could move the needle with more voluntary disclosure.

- Proxy advisors could just assume pay decisions were made at the start of the fiscal year unless told otherwise since that’s most US public companies' approach. That would require shifting their quantitative evaluations to be offset by one year.

Both approaches would help proxy advisors evaluate boardroom decision-making itself instead of the point-in-time performance evaluations under their current approach. This type of tweak might encourage boards to embrace the proxy advisor frameworks more fully rather than merely tolerate them.

Proxy advisors respond to what investors want. ISS and Glass Lewis are willing to rethink how they evaluate some parts of their executive pay frameworks because investors want them to. So now is a prime time for investors and companies to push for more sophistication.

Aligning pay evaluations with the timing and context of decisions wouldn’t require a dramatic overhaul—just a thoughtful adjustment from proxy advisors. It would be more accurate and more practical. The end goal here could be for proxy advisor evaluations to be actionable for investors and more practical for companies seeking to align executive pay with performance meaningfully.